We all want more money. But most Singaporeans get trapped in the weeds of personal finance because:

- It’s mind-numbingly boring: Understanding investments feels like reading the fine print of your insurance policy in a different language

- It’s ridiculously confusing: Everyone has a different hot take on where you should put your money, and they all contradict each other

- It’s often cringeworthy: I’m looking at you, financial gurus doing TikTok dances about compound interest

Most people think wealth-building is about finding the perfect hack. Cut back on bubble tea! Collect every Shopee coin! Time the crypto market! They spend hours trawling Reddit threads and finance blogs, hunting for tactics that might save them $20 or boost returns by 0.02%.

This is especially true in Singapore, where money conversations dominate everything. We get bombarded by property agent ads promising 20% returns. Every LinkedIn post is about side hustles. Entire industries exist just to educate, save, and invest your money.

But here’s my contrarian take: 95% of the tactics you read online don’t actually matter for growing your wealth.

Effective personal finance is like getting fit. You could try every fancy machine and obsess over the latest workout trends, but you’ll get 90% of the results with just a few basics: a barbell, some weights, and consistency. What you need is simple: Know what you want, set up your system, then move on with your actual life.

The 80/20 Rule Applied to Money

You’ve heard this before: Most people spend their lives obsessing over the 80% of actions that barely move the needle. Instead, if you nail the right 20% of actions, you’ll capture 80% of the results.

Your system doesn’t need to be perfect. It just needs to be enough.

After 10+ years of writing about money, I’ve finally consolidated my entire system into one place. This isn’t a comprehensive guide, and that’s exactly the point. I’m focusing on the Big Actions that actually matter for growing wealth, based on my experience.

(I’ve also linked to more detailed posts throughout this guide if you’d like to learn more. I’ll continue writing more posts to supplement this guide, so keep checking back for updates!)

Here are the three parts:

- Automate Your Money (so you never wonder “where did my salary go?”)

- Spend Strategically (focus on the big rocks, ignore the pebbles)

- Invest Without Stress (set it, forget it, get rich slowly)

This is a long post. Jump to whatever interests you most, bookmark it, and come back to it whenever you need.

(As always, this isn’t financial advice. I’m sharing what works for me and how it might help you. Do your own research, and don’t blindly follow my content!)

Part 1: Automate Your Money

Have you ever checked your bank account at the end of the month and thought, “Where the hell did my money go? How will I ever save for my BTO downpayment?“

There’s a better way. Instead of trying to keep track of every single dollar, set up a system that automatically directs your money where it needs to go. No willpower needed, no late payment charges, and no spending guilt.

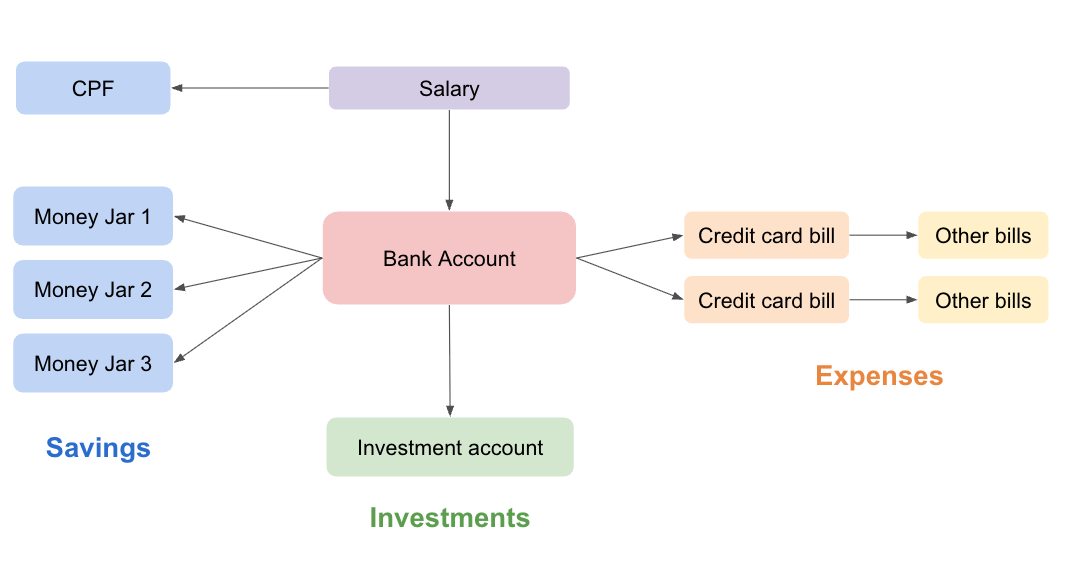

Here’s what mine looks like:

When my salary hits my bank account, it doesn’t stay there for long. My system automatically funnels portions toward savings, expenses, and investments. I never worry about whether I’m saving enough or if I forgot to pay a bill. You can read more about this system here.

Here’s how to build your own:

Set Up Your Money Jars

Most people dump everything into one savings account. This creates two problems:

- Spending guilt: Every purchase feels like theft from your future self

- No strategic direction: If you don’t know what you’re saving for or how much you need, how will you ever get there?

Solution: Separate your savings into different buckets. I call them Money Jars.

Find a bank account which allows for sub-savings accounts, like OCBC’s 360 account, MayBank’s iSavvy, or cash management accounts from Endowus or StashAway.

What Money Jars should you create? It depends on what your upcoming big expenses are. For example:

- BTO/condo downpayment

- Wedding fund

- Emergency fund (6 months of expenses)

- Learning fund (courses, books)

- Fun fund (guilt-free splurging)

Once you’ve created your jars, use online banking to set up recurring transfers for the day after your salary arrives. For example, if you get paid on the 25th, schedule transfers for the 26th:

- $1,200 → BTO money jar

- $400 → Emergency fund money jar

- $600 → Fun fund money jar

The best part: Once you’ve set up your Money Jar system, you never question whether you’re saving “enough” for your important expenses. The rest of your money becomes yours to spend, completely guilt-free.

Choose Your Credit Card Strategy

Credit cards serve two purposes:

- Earn rewards on spending you’re doing anyway

- Track expenses automatically

For rewards: Decide between cashback or miles. If you hate admin, pick a simple cashback card and you’ll generally get 1-3% back on what you spend. If you love travel and don’t mind juggling cards for different categories, miles can deliver much better value. I’ve used a general + specialised credit card strategy to fly on the Singapore Airlines Suites and Business Class for years, paying only a couple of hundred dollars in taxes.

The miles game changes constantly, so I follow The Milelion for updates. But if it feels like too much work, just stick with cashback.

For expense tracking: Stop manually logging expenses in spreadsheets. In Singapore, you can pay for 90% of things with cards + PayNow. Everything gets tracked digitally, so it becomes much easier to figure out what you spent on. Some banks even automatically categorise your expenses!

Set a monthly reminder to download your credit card statements. Five minutes of reviewing them will tell you where your money went and help spot fraudulent charges.

Automate Your Bills

The last step to set up your system is to simply automate all your payments. It drives me crazy when I hear how people are still paying their bills manually with AXS every month. If you’re doing the same thing over and over, automate it! You have better things to do with your time. Here’s how:

Step 1: Set all bills (e.g. Netflix, utilities, insurance, gym, data plan, etc.) to auto-pay via credit card. You earn rewards on spending you’d do anyway.

Step 2: Auto-pay your credit card bills from your bank account. This ensures that you’ll never miss a payment, and never have to pay interest or late fees.

Pro tip: Set an annual calendar reminder for when your credit card annual fee hits. Call and ask them to waive it. Some banks like UOB can be sneaky in the way they charge fees—don’t let them get away with it!

The End Result: Peace of Mind

Think about the thousands of micro-decisions about money you make monthly: Should I splurge on dessert? Did I pay my credit card? How much should I spend on travel?

This system eliminates decision fatigue. You’ll save hundreds of hours over your lifetime and never incur another late fee. More importantly, you’ll know exactly where every dollar goes, letting you make strategic adjustments. For example, are you falling short on saving up for your car? A quick glance at your statements will show you exactly where to cut back.

Having these systems gives you hard-won peace of mind that your finances are running themselves—automatically.

Part 2: Spend Strategically

Now that your money is automatically flowing where it needs to be, let’s talk expenses. Don’t worry—I’m not here to guilt-trip you about $7 bubble teas or taking Grab versus MRT.

The truth: Small expenses like these don’t matter for long-term wealth.

Instead, I’m focusing on spending categories that actually make a difference: your milestone expenses, your insurance payments, and taxes. If you can save even 1-2% on each of these, they’ll be worth more than all your bubble teas or Grab rides combined.

Let’s get to it:

Afford Your Milestones

Throughout your life, you’ll likely hit several expensive milestones like property, wedding, car, or kids. Most Singaporeans wing it when it comes to these big expenses: They save what they can and hope it’s enough when the time comes.

You’re already ahead because you’ve set up Money Jars. But if you’re taking on debt for these milestones—like a mortgage or a car loan—be strategic.

My rule of thumb: The debt should be manageable even if you lose your job for 6 months.

For example, I follow the 3-3-5 Rule when it comes to property:

- 30% down: Your initial capital should be at least 30% of the property price

- 1/3 of salary: Monthly mortgage shouldn’t exceed one-third of your income

- 5x annual income: Purchase price can’t exceed five times your annual income

These seem conservative, but they prevent you from overstretching yourself while still using debt strategically.

Buy Just Enough Insurance

Insurance agents love positioning insurance as a wealth-building tool, encouraging their clients to overinvest. It’s not.

Insurance is just a way to manage your risks, nothing more. See this article from MoneyOwl on why insurance is like a fire safety system. There’s no point in buying an expensive, state-of-the-art system when all you need is a cheap fire extinguisher.

Most young Singaporeans will only need 3 types of insurance:

- Hospitalisation: Your biggest risk is a massive medical bill which you can’t afford. Hospitalisation plans are cheap when you’re young, and heavily regulated to make sure you’re getting a fair deal. Go for the most premium plan you can afford, since you can also use your CPF Medisave to pay for most of it.

- Disability Income: Your second biggest risk is being unable to work. A disability insurance plan pays you an income if you’re disabled. Keep premiums manageable by moderating your coverage to your monthly expenses, not your entire income.

- Term Life: If people depend on you financially (e.g. a child or aging parents), get cheap term insurance. Skip the expensive whole life or investment-linked plans. Add a Critical Illness rider if you want coverage for major health expenses. Life insurance isn’t absolutely necessary if you don’t have any dependents (e.g. if you’re single with no kids, and your parents have their retirement sorted out).

A young person can cover all three for a few hundred dollars monthly.

Insurance agents will often push more comprehensive (expensive) plans. Stay focused on buying the right-sized “fire extinguisher” for your life.

Save Money on Taxes

Singapore’s income taxes are among the lowest in the world. But as your income grows, taxes will start to hurt. Here’s how to minimise them:

Top up CPF: You can enjoy up to $8,000 in tax relief annually by making cash top-ups to your CPF account, and an additional relief of $8,000 for top-ups to your loved ones’ CPF accounts. By topping up your CPF-SA, this money goes to your future self while earning a risk-free 4% return. It also helps you to meet the Full Retirement Sum and unlock Singapore’s best-kept secret for wealth-building.

Use SRS: Next, contribute up to $15,300 yearly to your Supplementary Retirement Scheme (SRS) for tax deductions. Even if you need the money before retirement, you’ll only pay a 5% penalty plus taxes. Open an account now and deposit a small amount—say $1—into it. Why? So that you can lock in the age when you can withdraw your funds (the current retirement age when you made your first contribution).

Donate to charity: Donations qualify for 250% tax relief, which means if you donate $100, you can deduct $250 from your taxable income. This isn’t a money-saving hack (since the amount you donate will always be more than the taxes you save), but if you believe in giving back, giving.sg is one of my favourite platforms to make a donation seamlessly.

The End Result: Spend Guilt-Free

Most people feel guilty about spending. They’ll skip their afternoon coffee or feel bad about Sunday brunch. This is no way to live.

By handling the big rocks—milestones, insurance, taxes—you’ve optimised what actually matters. As long as you’ve taken care of savings, investments, and major expenses, spend the rest however you want.

Want to splurge money on a Business Class ticket? Sure thing. Go for a $700 dinner date? Enjoy yourself! Money isn’t just meant to be hoarded—once you’ve taken care of your responsibilities, don’t worry about spending it on what you love.

Part 3: Invest Without Stress

Inflation will erode your savings, and your income won’t grow forever. Investing is the surest, most sustainable way to grow your wealth over the long term.

However, investing is also the one area that’s most susceptible to hype and BS. Every day, we’re bombarded with news about the stock market, and your friends are constantly telling you how much they made from crypto. The good news is, much of what you see in the media doesn’t really matter to us.

Real investing is about: 1) Having a clear goal, 2) Adopting a passive investing approach, and 3) Staying the course over the long term.

Set Your FIRE Number

Let’s be clear: You won’t get rich overnight. Anyone promising huge returns quickly is running a scam or asking you to take extreme risks.

But you can build significant wealth by investing early and consistently over 20-30 years. For example, if you started with $10,000 and invested $500 a month at 6.8% real returns (the stock market’s long-term return after inflation), you’ll have over $600K in 30 years. Probably much more as your income—and monthly investments—increase. You can calculate your own projections using this calculator.

What’s your end goal? For most people, it’s to become Financially Independent and Retire Early (FIRE). To calculate your financial independence number, use the 4% Rule: Take your annual expenses and multiply them by 25.

For example, if you need $4,000 monthly to live comfortably, that’s $48,000 yearly × 25 = $1.2M for financial independence.

This number will evolve as your needs change, and that’s okay. The point is to make your goal concrete. Financial independence is actually very achievable—not the crazy amounts most people imagine.

Invest in the Market (Not Individual Stocks)

The most reliable long-term investments are the stock and bond markets. Notice that I said the stock market, not individual stocks.

Why? It’s extremely difficult to pick winning stocks, but markets trend upward over the long term. This is called passive investing, which means tracking the whole market instead of trying to beat it.

Research consistently shows that 75% of professional fund managers don’t beat their benchmarks over 5 years. If professionals struggle to pick winners, there’s little chance that you and I can do better.

Logic: If most professionals can’t beat the market, the best way to beat most professionals is to… invest in the market!

How can you get started? The easiest way is to use a robo-advisor like Endowus, Syfe or StashAway. You can start with $100 monthly and they’ll help you to automate everything: your asset allocation, tracking your portfolio, and so on.

You can also build your own passive ETF portfolio for lower costs, but it’s complex. You’ll need to handle rebalancing, dividend reinvestment, and other admin. For new investors, roboadvisors are worth the slightly higher fees.

Invest Consistently and Ignore the Noise

Tell me if this sounds familiar: “The market is overvalued!” “Tech stocks are in a bubble!” “Cash is king right now!“

The media (and your crypto bro friends) love to make you constantly anxious and wondering when the “right time” to invest is. None of this matters, because nobody can predict when the markets will go up and down in the short term. Read the news for entertainment if you have to, but don’t rely on it to make investing decisions.

There’s an old investing adage: It’s not about timing the market; it’s time IN the market.

To make the most of index investing, ignore the noise and simply invest consistently. The best way is to use dollar-cost averaging: Invest the same amount at the same time every month, regardless of market conditions. Why this rules-based approach works:

- It helps you overcome the fear of buying when prices feel “too high”, or when markets crash

- When prices are high, your money buys fewer units. When prices are low, you buy more units

- Using this approach, you accumulate more units at a lower average price

How to dollar-cost average:

- If you’re investing through a roboadvisor: Set up automatic monthly transfers and they’ll handle everything else.

- If you’re investing manually through ETFs: Do some simple math. Want to invest $1,000 monthly in VRWA at $140? Buy $1,000 ÷ $140 = 7 units (rounded down). Repeat monthly, adjusting the number of units you buy based on the current price.

Do this consistently and be patient. Remember: This is a long-term investment.

The End Result: Stress-Free Investing

Once you’ve set up your automated investing system, something magical happens: You stop caring about daily market movements. Your friends might panic about tech stock crashes or get FOMO about the latest crypto surge, but you’ll just shrug and go back to living your life.

You’ll check your portfolio maybe once a quarter, not because you’re neglecting it, but because there’s literally nothing to do. Your money grows quietly in the background while you focus on your career, relationships, and actual experiences.

This is what financial peace of mind looks like—not obsessing over every market fluctuation, but knowing your system is working even when you’re not watching.

Conclusion: Don’t Focus on Money

So there you have it—everything I know about personal finance in Singapore, compressed into one guide.

A personal story: When I started working, I was obsessed with money. I read every article, bought every book, tracked expenses obsessively in Excel. But this came at a cost—focusing too much on money meant neglecting family and other parts of life. I was constantly stressed about unexpected expenses or when my “perfect” system had hiccups.

It was only when I faced a personal crisis years later that I realised I had hit rock bottom. I had obsessed over building my dream life so much, that I had forgotten how to live my actual life.

That’s why I wrote this post: Personal finance doesn’t have to be perfect. You just need something “good enough”—something workable that handles your money so you can move on with living.

Money is an enabler, not the destination. If you mess it up, you can always earn more. Having more or less of it doesn’t make you more or less of a person.

Set up something that’s “good enough,” then focus on what really matters: living a truly rich life.