My arms are sticky with sweat as the crowd murmurs around me. My shoes pad softly on the damp grass of Hong Lim Park. I swat a mosquito on my arm just when someone next to me yells, “Abolish the CPF! Return our money!!”

It’s 7 June 2014. I’m at the #ReturnOurCPF protest held at Hong Lim Park. I didn’t know much about CPF back then, but it was rare to experience a protest in Singapore, so I decided to check it out.

The emotion was palpable. People were really pissed about the CPF system. They felt that their hard-earned money was wrongfully locked away, and there were conspiracy theories circling that the government was using the CPF to cover losses from poor investments.

Many of these frustrations and anxieties stemmed from the fact that most people – myself included – didn’t really understand the CPF system. It had complex rules and qualifications, and the CPF Board didn’t do a great job back then at communicating WHY those rules were in place.

Fast forward to today. To the government’s credit, they made several improvements to the CPF system and stepped up their game at communicating the benefits to the public.

But not everyone’s making full use of them.

My CPF Wake-Up Call

For many of my friends, CPF feels like that gym membership you never use but can’t cancel. 20% of your salary is automatically deducted every month for something that you’ll maybe benefit from decades later. You know it’s probably good for you, but right now it just feels like money disappearing into some secret vault somewhere.

For years, I was just like them. I dutifully made my contributions. Used some for housing. But otherwise, I basically ignored it. The whole system felt like a maze designed by bureaucrats who enjoyed making things unnecessarily complicated.

Then several years ago, during ICT (because where else do life-changing conversations happen?), my army buddy and I started chatting about personal finance. I was complaining to him about CPF over kopi-o kosong.

He laughed and said, “You know that you’re sitting on Singapore’s best-kept investment secret, right?”

He was right.

As I researched more, I realised that CPF – specifically the CPF Special Account (CPF-SA) – could accelerate my progress towards FIRE. This “boring” government scheme might be one of the most powerful wealth-building tools that I’d never thought of.

Why the CPF-SA Is Singapore’s Most Exclusive Investment

Picture this: You get a call from your private banker. She offers you an exclusive chance to buy into an investment. The investment return outperforms cash account interest rates in London, New York, and Zurich. Furthermore, unlike global bond indices, this investment is risk-free, backed by a triple-A credit entity who offers an explicit guarantee. If you want, you can add more funds into it and boost your return even further.

This is essentially what the CPF-SA is!

First, the CPF-SA offers an “exclusive investment” that only Singaporeans & PRs can access.

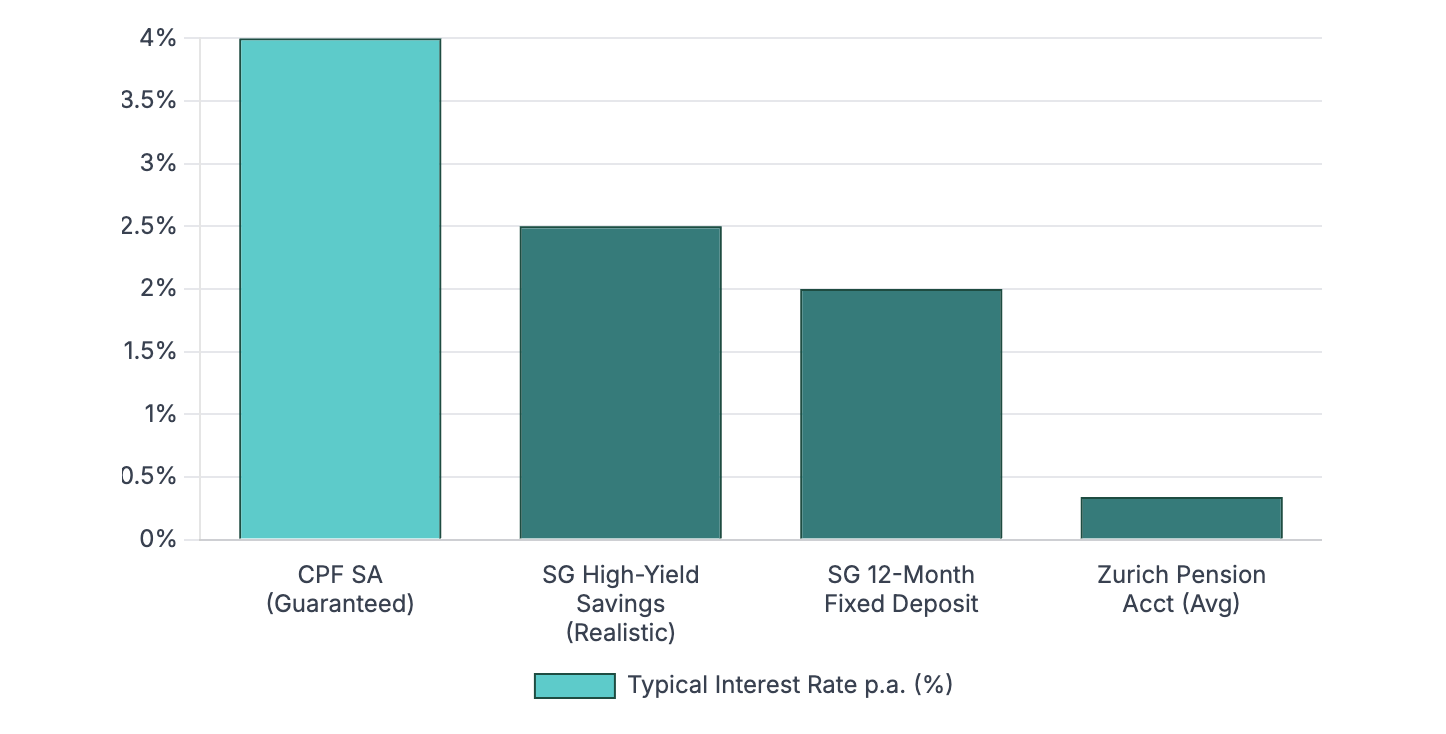

As we know, the CPF-SA offers a guaranteed 4% interest rate. This is much higher than other typical deposit or savings yields:

While international investors scramble for safe yields above 2%, Singaporeans & PRs have access to a risk-free 4% return that’s backed by the Singapore government.

Foreign wealth managers would kill to offer their clients a guaranteed 4% return. Yet most Singaporeans treat this exclusive access like an inconvenience.

Second, topping up your CPF-SA delivers an immediate “return” for through tax relief.

Aside from your regular CPF-SA contributions, you can also top up your SA through the Retirement Sum Topping Up Scheme. This allows you to enjoy up to $8,000 in tax relief by making cash top-ups to your own CPF accounts, and an additional $8,000 by making cash top-ups to your loved ones.

Let’s say that your marginal tax rate is 10% and you top up $8,000 into your CPF-SA. Your top-up gives you an $800 immediate relief (based on your 10% tax rate) + $320 in first-year interest (based on the 4% interest rate) = $1,120 total first year benefit.

That’s a 14% total rate of return on your $8K!

For high-income earners who pay a higher tax rate, their “returns” through tax reliefs are even higher.

“But My Money Is Locked Up & The Goalposts Keep Moving”

Despite these attractive returns, many people don’t see the CPF as a proper “investment” since it comes with so many restrictions. For example:

- You can’t access the funds until your 55th birthday

- Even then, your CPF funds can’t be used as you wish – they must be used to purchase a CPF Life plan

- You can only withdraw your CPF funds above the Full Retirement Sum (FRS)

Then there’s the frustration about “moving goalposts” because the FRS keeps increasing with inflation:

Having an FRS that keeps growing every year feels like you’re running a race where the finish line keeps getting pushed further down the track.

I get it. I felt this frustration too. But consider a slight reframe:

The FRS: Your Liquidity Unlock Milestone, Not a Constraint

Don’t see the FRS as a constraint. Instead, think of it as a threshold to hit.

The earlier you can hit it, the faster you can unlock real-life benefits. Here’s why:

Hitting the FRS unlocks flexibility for your CPF funds

Every dollar above the FRS becomes withdrawable once you turn 55. Think of it as your money being held in a high-security vault, but once you prove you’ve got enough for retirement (the FRS), the vault opens up for the excess.

For example, let’s say you’ve got $500K in your CPF at 55, and the FRS is $300K. While the $300K FRS will be used to purchase your CPF Life plan, the extra $200K is yours to do whatever you want with.

Therefore, hitting FRS early (before 55) fundamentally changes the nature of all future CPF contributions. Anything above the FRS can be seen as part of your investment portfolio – fully accessible after you turn 55.

Once you hit the FRS, it becomes self-sustaining

Yes, the FRS increases with inflation each year. But this increase is lower than the 4% interest in your SA.

For example, the FRS will increase by 3.4% from 2025 to 2026, and 3.5% from 2026 to 2027.

In other words, once you hit the FRS in your SA, your SA balance should naturally pace in line with the FRS, even if you never contribute another cent.

Think of it like this: Hitting the FRS in your SA is like stepping onto a moving escalator. Even if you never take another step, you’ll still stay ahead of the rising steps.

SA contributions above the FRS are invested into an “invisible 4% bond”

Once you hit the FRS early, you can effectively treat all subsequent mandatory SA contributions as a “risk-free 4% bond” whose principal becomes available to you at 55.

Why? Because you know that when you turn 55, you can withdraw all funds plus the interest you earned above the FRS. This redefines your SA from a locked-up fund to a high-yield asset post-FRS.

Personally, I count my SA savings as part of my bond portfolio, since I can count on it to reliably generate 4% a year for me.

Hitting FRS also provides the psychological and financial freedom to take more calculated risks with your non-CPF investments. You know your basic retirement is already covered via your future CPF Life payouts, so you can afford to be more aggressive with your other investments (within reason!)

Cash Top-Ups: How to Accelerate Your Path To The FRS

Okay, so you want to hit the FRS. How do you do it?

First, continue with your mandatory SA contributions since this forms the base of your SA savings.

Then, with any excess funds – top up your SA (or RA if you’re above 55) with cash. For many years, I topped up to the maximum amount ($8,000 this year) to enjoy tax relief. By doing this, you get:

- Immediate tax relief of up to $8,000 a year (money in your pocket now)

- 4% guaranteed returns (better than most “safe” investments)

- Compound growth over time (the eighth wonder of the world)

What if you’ve already hit your FRS?

If you’ve already hit your FRS, unfortunately CPF won’t let you top up your SA any further. That means you won’t get to enjoy tax relief on this portion of your money going forward 😭.

However, the good news is that any mandatory CPF contributions (i.e. from your salary and employer contributions) will still flow into your SA.

And like I mentioned, this is the pot that you’ll get to withdraw when you turn 55.

Other approaches to hit the FRS, but use with caution

There are two other possible methods to achieve the FRS, but I don’t personally practice them for the following reasons:

- OA-to-SA transfers: You can also transfer funds from your OA to SA to enjoy a higher interest rate (4% in your SA vs 2.5% for the OA), but remember that this is irreversible! If you need the money in the future, there’s no way to get it back. Plus, many of us need our OA funds for more immediate needs like servicing our mortgages or loans, so you should only consider this if you have significant excess OA funds gathering dust.

- CPFIS-SA investments: You could also consider investing your CPF funds via the CPFIS, potentially getting a higher return. However, like I said earlier, getting a 4% risk-free investment is almost unheard of. I also find the CPFIS extremely finicky and cumbersome: There are restrictions on what you can invest in, and you can only execute it on a few platforms. Personally, I choose to save myself the trouble and leave my CPF-SA funds earning the default 4% a year. For my riskier investments, I choose to use cash instead.

The Bottom Line

CPF isn’t sexy. It doesn’t have the thrill of picking stocks or the excitement of crypto.

But it’s reliable, it’s guaranteed, and it works.

Most Singaporeans treat CPF like that gym membership they never use – paying for it but not maximising its benefits. Don’t be like them.

The FRS isn’t just a government benchmark; it’s your baseline for your retirement portfolio. Hit it early, and you’re not just securing your retirement lifestyle. You’re building a foundation that gives you options, flexibility, and peace of mind.

PS: I know it sounds like it, but this isn’t a sponsored post by the government or anything. It’s just a topic that I think deserves more attention!