Most people manage their money the same way they managed it 20 years ago: manually, one transaction at a time.

They get their salary, and it just sits in one account. When bills arrive, they log into different websites to pay them. When they want to save for a holiday, they try to remember to transfer some money. When they think about investing, they spend weeks agonizing over the “right time” to start.

It’s exhausting.

I know because I used to be the worst version of this. 15 years ago, I used to obsessively log every single expense into an app. $1.50 kopi? Logged. $4 chicken rice? Logged and categorized. I was making 8-10 entries per day, spending 30 seconds each time deciding whether my bubble tea was “Food” or “Entertainment.”

The breaking point came during dinner at Les Bouchons. My then-girlfriend was excitedly telling me about her holiday in Oxford when I interrupted her mid-sentence to pull out my phone to log our $19.90 cocktails.

“Are you even listening to me? Stop being so cheap!”

She was right about me not paying attention. But I wasn’t being cheap, I was just mentally exhausted from trying to manually manage every dollar that came in and went out.

Here’s what I realized: all this manual effort wasn’t making me richer. It was just making me tired.

The Mental Load of Manual Money Management

Think about how many money-related decisions you make in a typical week:

- Should I transfer money to T-Bills this month?

- Did I pay my credit card bill?

- Is now a good time to invest, or should I wait?

- How much have I spent on dining out?

- Can I afford this weekend trip?

- Should I top up my investment account?

Each decision burns mental energy. And unlike big decisions that matter (like which job to take, whether you should get married, how to spend more time with your kids), these are small, repetitive decisions that you’ll make again next week, and the week after that.

It’s like having to remember to breathe. Technically possible, but why would you want to?

A Better Way: Let Technology Handle the Boring Stuff

There’s a better approach, and it’s called systems thinking. Instead of relying on willpower and memory to manage your money, you use technology to make good financial choices automatically.

Think of it like this: You don’t manually decide when your phone backs up to the cloud, or when your Netflix subscription renews, or when your work laptop installs security updates. These things just happen in the background, freeing you to focus on more important stuff.

Your money can work the same way.

The idea isn’t complicated: set up simple, automated processes that handle your routine financial tasks so you don’t have to think about them. Pay bills automatically. Save money automatically. Invest automatically.

When Ramit Sethi wrote about this concept in “I Will Teach You To Be Rich,” it completely changed how I thought about personal finance. But his system was built for Americans with their 401(k)s and Roth IRAs. So I adapted my own system for Singapore’s context:

Here’s how each piece works.

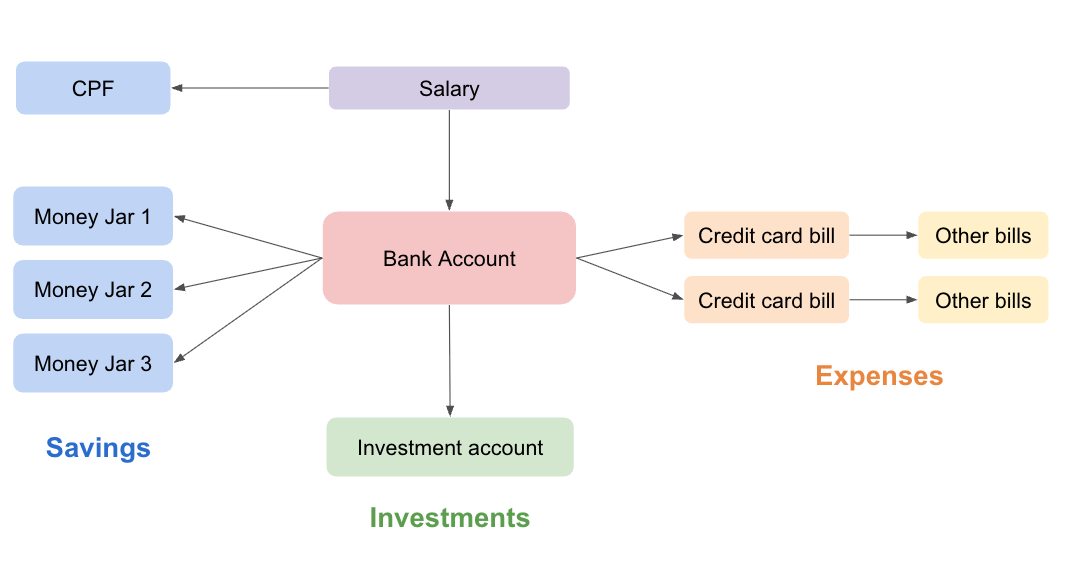

Your Main Bank Account: The Distribution Center

Most people treat their bank account like a storage closet—everything just piles up in one place. But this creates problems:

- Every purchase feels guilty because you’re taking money away from your future goals

- You can’t track progress toward specific things like your property downpayment or vacation fund

- It’s risky to keep everything in one place (anyone can get scammed these days)

Instead, treat your main account like a distribution center. Money comes in from your salary, gets sorted automatically, and goes out to where it needs to be.

I use OCBC’s 360 Account for this, mainly because their Savings Goals feature makes it easy to separate different pots of money. When my salary hits on the 25th, the money doesn’t stay there long. By the 26th, everything has been automatically moved to its proper place.

Your Savings: Separate Buckets for Different Goals

Here’s where most people’s money management falls apart. They’ll say “I’m saving for a house and a wedding and an emergency fund,” but it’s all just one number in one account. Mentally, it’s impossible to track progress on multiple goals at once.

The solution: separate buckets (or “Money Jars”) for each goal, with automatic monthly transfers. I wrote more about this here.

An example setup:

- Emergency fund: $400/month (building up to 6 months of expenses)

- Learning fund: $200/month (for courses and books)

- Fun fund: $300/month (guilt-free spending money)

Each bucket gets filled automatically the day after my salary arrives. When I want to book a weekend getaway, I just check my fun fund. If there’s money there, I can spend it without any guilt. If not, I wait until next month.

It’s like having a financial assistant who never forgets and never judges your choices.

Your Bills: Set Them to Pay Themselves

Stop paying bills manually. If you’re still logging into six different websites every month to pay your utilities, Netflix, gym membership, and credit cards, you’re doing it the hard way.

Here’s the simple setup:

- Step 1: Put all your bills on auto-pay using your credit card

- Step 2: Set your credit card to auto-pay from your bank account

- Step 3: Review your statements once a month (takes 2 minutes) to catch any weird charges

But be warned: Setting up GIRO can sometimes be a hassle. Most companies now let you do it online, but a few (I’m looking at you, UOB) still need you to fill in a paper form and mail it back to them.

But here’s the thing: it’s worth the one-time hassle. 30 minutes of paperwork in exchange for never having to think about bill payments again? That’s a great trade.

Pro tip: Keep about a month’s salary in your main account as a buffer. I learned this the hard way during Christmas when my credit card bill spiked from all the gift shopping and end-of-year dinners.

Your Investments: Same Amount, Every Month

People spend way too much time trying to figure out the “perfect” time to invest. Market going up? “It’s too expensive now.” Market going down? “Maybe it’ll drop more.”

This kind of thinking keeps people on the sidelines for years while their money earns practically nothing in the bank.

The better approach: invest the same amount every month, no matter what’s happening in the markets. Some months you’ll buy when prices are high, some months when they’re low. Over time, it averages out.

My system automatically invests the same amount on the 27th of every month into an Endowus Flagship portfolio of 80% equities and 20% bonds. (This is slightly aggressive for my age because I’ve been investing for 15+ years and can handle the ups and downs.) The money gets withdrawn, invested, and rebalanced automatically. I just check the performance quarterly to make sure nothing’s broken.

If you’d like to start with Endowus, here’s a referral code where you and I can get $100 off in fee credits.

The Life-Changing Result: Mental Freedom

Here’s what happened after I set up this automated system: I got my brain back.

Before, I was constantly thinking about money. Not big-picture wealth-building thoughts, but tiny administrative tasks: “Did I pay that bill?” “Should I transfer money to savings?” “Is this a good time to invest?”

Now, my monthly money management routine takes exactly 5 minutes:

- Check that my salary deposited correctly (30 seconds)

- Scan credit card statements for anything weird (2 minutes)

- Glance at investment performance (2 minutes)

- See how my savings goals are progressing (30 seconds)

That’s it. Everything else runs on autopilot.

The mental space this creates is incredible. Instead of thinking about money 20 times a day, I think about it once a month. All that freed-up brainpower goes toward things that actually matter: getting better at my job, spending quality time with people I care about, working on side projects.

How to Build Your Own System

Ready to stop manually managing every dollar? Here’s your game plan:

Week 1: Set up your Money Jars: Use your bank’s savings goals feature or open separate savings accounts. Figure out how much you want to save for each goal, then set up automatic transfers for the day after you get paid.

Week 2: Start the bill automation paperwork: Begin setting up GIRO for all your regular bills. Yes, it’s annoying. Yes, it takes forever. Do it anyway. This is a one-time pain for permanent gain.

Week 3: Automate your investing: Pick a platform (e.g. Endowus, StashAway) and set up automatic monthly investing. Don’t overthink the perfect strategy—consistency beats perfection.

Week 4: Test everything: Run through a full month to make sure money flows where it should, bills get paid automatically, and your investments execute properly.

The Unexpected Bonus

Six months after setting this up, my wife (yes, the same girlfriend from the start of this post) wanted to book a last-minute trip to Bangkok.

In the old days, I would have spent 15 minutes checking balances, calculating impacts on other goals, and generally making it way more complicated than it needed to be.

With the new system, I just checked our travel fund. Money was there. Trip booked. Zero stress.

“This is so much better than watching you log every coffee purchase,” she laughed.

She was right. The automated system didn’t just improve my finances—it improved my relationships and peace of mind.

The Big Picture

The best money management system isn’t the one that tracks every dollar you spend. It’s the one that removes money decisions from your daily life so you can focus on the things that actually make your life better.

Think about it: successful people don’t spend their time on repetitive, low-value tasks. They build systems to handle the boring stuff automatically, then use their mental energy for high-impact activities.

Your money should work the same way.

The goal isn’t to become a financial micromanager. It’s to set up simple systems that handle your money responsibly while you focus on building the career, relationships, and life you actually want.

Now if you’ll excuse me, I’m going to grab some bubble tea. And unlike 15 years ago, I won’t be logging it anywhere.

What’s the most annoying money task you’re still doing manually? Let me know in the comments. Let’s brainstorm if we can automate it.